The End of Expert Synthesis: Why Raw Visual Data Just Became Your Most Valuable Asset

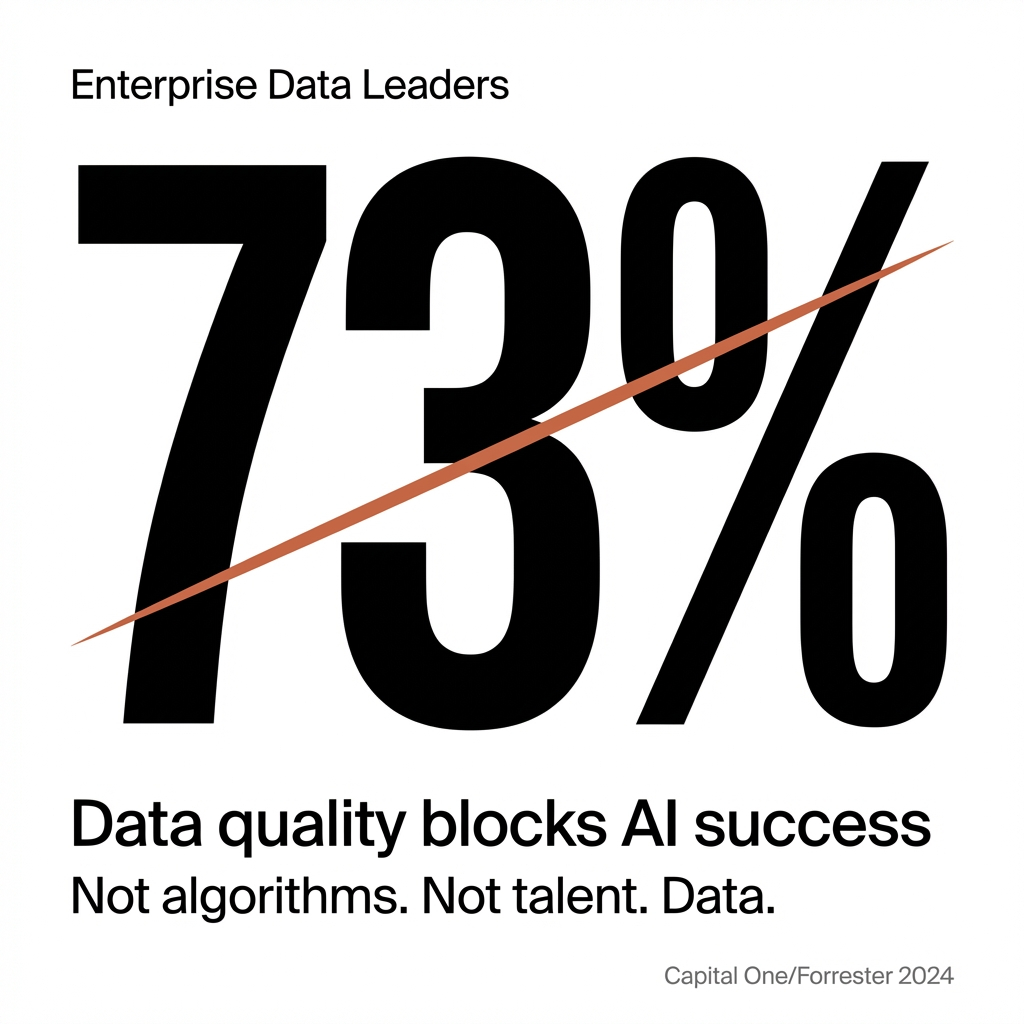

73% of enterprise data leaders identify "data quality and completeness" as the primary barrier to AI success

Ranking it above algorithms, computing costs, and talent shortages.

— Capital One/Forrester Research, 2024

Over 60% of AI projects fail. Not because of bad algorithms. Because of bad data.

While insurance carriers pour billions into AI platforms, the real problem isn't the technology. It's the foundation they're building on: incomplete, biased, expert-filtered data sitting in PDFs that can't train AI systems effectively.

For commercial insurance brokers, this creates an enormous opportunity that almost nobody sees.

For decades, insurance underwriting has operated on a simple premise: Send an expert to a property. Let them decide what to photograph, what to measure, what to write down. Then read their report and make decisions based on their synthesis.

We told ourselves this was the best way to assess risk.

It wasn't.

It was the only way that was physically possible given human bandwidth constraints. You couldn't bring every underwriter, every claims adjuster, every decision-maker on-site to spend days documenting every square foot of a property. So we sent one person with a camera and a ladder, and we accepted their filtered, sampled, subjective view as "truth."

That constraint just disappeared.

As an insurance broker and damage advocate who has handled large loss claims as a contractor, I've watched millions get spent arguing over what an expert wrote three years ago. I've seen brilliant brokers lose accounts because they couldn't prove what their policyholders could only assert based on someone's 20-page PDF.

Here's the paradigm shift nobody's talking about: Written reports can't scale as the foundation for verifiable truth.

Experts are absolutely essential. But asking them to spend hours writing comprehensive text reports trying to capture every detail of a property? That's the bottleneck. No expert can document everything in writing. They're forced to sample, to prioritize, to synthesize what they think will matter later.

The raw visual documentation that we used to throw away after the expert wrote their report? That's now the foundation. The expert analysis is still critical, but now experts can analyze comprehensive visual data instead of trying to capture and describe everything in text.

Written reports based on incomplete visual sampling can't serve as verifiable truth. They're samples. Interpretations. Not comprehensive documentation of reality.

And most commercial insurance brokers don't even realize the game just changed.

The Dual-Layer Asset Nobody Sees

Understanding this paradigm shift from expert synthesis to raw visual data reveals why early-moving brokers are building compound advantages.

When you deliver Property Blockchain™ methodology to your clients, you're building two distinct assets simultaneously:

Layer One: Immediate broker advantage. You become the broker who eliminates the 3-6% ambiguity margin in every policy. You're the one who walks into carrier presentations with comprehensive visual documentation instead of limited sampling reports. You change underwriter conversations because you bring verifiable visual truth that experts can analyze, not summaries of what one inspector thought mattered.

Layer Two: Future AI infrastructure. This is the layer your competitors will miss until it's too late.

Every Capture Block™ you create becomes foundational data that experts and AI systems can analyze for insurance decisions. Not data built on incomplete sampling and written summaries. Data built on comprehensive visual documentation of actual property conditions.

The carriers and MGAs that have visual data libraries will be able to price risk accurately. The brokers who bring those visual libraries to the table will win the accounts.

The brokers still showing up with traditional inspection PDFs will find themselves uncompetitive on pricing and unable to prove the value they claim to deliver.

The 3-6% Margin That Exists Because Underwriters Price Opinions, Not Reality

Here's something most brokers understand intuitively but rarely articulate clearly:

A scared underwriter is an expensive underwriter.

When an underwriter can't verify actual property conditions (when all they have is an expert's filtered synthesis from a site visit two years ago), they build in safety margins. They have to. Information asymmetry is at the heart of insurance market pricing inefficiencies.

Think about how rating actually works. Actuaries use losses per zip code, losses per neighborhood, radius rating around catastrophe zones. They can't get granular to the property level because they don't have verifiable, current, comprehensive property-level data.

They have written summaries of limited site visits sitting in PDFs.

So if your client's building is impeccably maintained with a brand-new roof and updated systems, they still pay nearly the same rate as the poorly maintained building three blocks away. Because the underwriter is pricing based on geographic loss data and an inspector's summary, not on verifiable reality.

That's the 3-6% margin. It's the cost of making underwriting decisions based on limited sampling reports instead of comprehensive visual documentation.

Now imagine being the broker who walks into carrier negotiations with complete visual documentation of every square foot of your client's property. Not an inspector's opinion about what mattered. Not a sampling of photos someone decided to take. Every square foot. Interior and exterior. Time-stamped. Queryable.

What happens in that conversation?

The underwriter's fear evaporates. They can verify actual conditions themselves instead of trusting someone's written summary. They can see the roof condition from every angle. They can inspect HVAC units from all sides. They can verify fire safety systems, building envelope integrity, maintenance quality.

You just became the broker who replaces opinion with verifiable facts. That's worth 3-6% in pricing power.

Why We Accepted Expert Synthesis in the First Place

Let's be honest about what traditional property documentation really is.

An inspector goes to a site with a camera and a ladder. They spend 2-4 hours there. They photograph what they think is important based on their training and the scope they were hired for. Then they go home and write a report synthesizing what they saw into text.

That report becomes "truth."

But here's what that report actually represents: One person's professional assessment of which 0.1% of the property they had time to document and what they believed it meant.

We didn't choose this system because it was optimal. We chose it because bringing every stakeholder on-site for days to document everything was impossible. You couldn't get the underwriter, the risk engineer, the claims adjuster, the facility manager, and the CFO to all spend a week at the property capturing every square foot.

So we sent one expert and accepted their written summary as the best proxy for reality we could afford.

That was a bandwidth problem, not a quality decision.

The paradigm is shifting from written reports to comprehensive visual documentation as the foundation.

Here's why this changes everything: When you have complete visual documentation, experts can analyze it across unlimited dimensions (roofing specialists, HVAC engineers, life safety consultants, ADA compliance experts, whatever expertise you need). AI tools can assist with pattern recognition and initial assessment, but expert judgment remains essential.

What you can't do is expect a single inspector to write comprehensive reports anticipating every future question. What you can do is capture everything visually, then bring expert analysis to bear on whatever questions arise.

Written reports based on incomplete visual sampling can't serve as comprehensive truth.

When you base underwriting decisions on an inspector's 40-page PDF, you're not basing it on property reality. You're basing it on what one person decided to look at, happened to notice, and chose to write down.

That's why Gartner predicts that through 2026, organizations will abandon 60% of AI projects unsupported by AI-ready data. The AI isn't the problem. The underlying data (built on written summaries of limited site visits rather than comprehensive visual capture) is the problem.

Sixty-three percent of organizations either do not have or are unsure if they have the right data management practices for AI. That's because their "data" is actually just written summaries sitting in PDFs, not comprehensive visual documentation.

This is the unlock: When you have complete visual documentation (every square foot, interior and exterior, captured in navigable Digital Twins with geotagged HD imagery), experts can analyze whatever matters when it matters.

What does the carrier's roofing specialist need to see? Pull it up. Show them every penetration, every seam, every condition indicator for their expert assessment.

What does the underwriter's HVAC engineer want to verify? Show them every unit from all sides with model numbers visible so they can apply their expertise.

You're not hoping an engineer happened to write about the specific detail that matters now. You're showing them comprehensive visual documentation so they can apply their expertise to current questions.

The brokers building visual data libraries today are building the foundation that makes AI actually work. That foundation will dominate the industry by 2027.

How This Changes the Underwriter Conversation

I've presented Capture Block™ documentation to underwriters who are used to receiving traditional submissions. The inspector's PDF. The engineer's written report. The text-based summary.

Once the light bulb goes off in their heads, everything changes.

They realize they're no longer dependent on what one inspector chose to document in writing. They can verify conditions themselves using their own expertise. They can pull up any aspect of the property and inspect it directly instead of hoping someone happened to photograph and write about the specific detail they care about.

This is the shift from relying on written summaries to having comprehensive visual documentation for expert review.

The underwriter can engage with the Digital Twin as deeply as their rating guidelines require. Need to see all roof penetrations? Pull them up and apply your roofing expertise. Want to verify HVAC maintenance based on visible corrosion or lack thereof? Look at every unit from every angle using your HVAC knowledge. Concerned about a specific exposure mentioned in loss runs? Navigate to that area and inspect current conditions yourself.

You're not asking them to trust a written summary. You're giving them comprehensive visual data so they can apply their own expertise.

Here's what I see coming: Underwriters recognizing that properties with active Capture Block™ programs deserve preferred pricing because the fundamental nature of the risk has changed.

When every square foot is documented interior and exterior, you eliminate litigation vectors. Litigation exists to resolve ambiguity. When you have comprehensive, unbiased visual documentation captured pre-loss, there's nothing to litigate.

Was the roof in good condition before the storm? Here's the Capture Block from 60 days prior showing every square foot.

Did the water damage start before or after the covered event? Here's the interior 360-degree documentation showing no pre-existing water intrusion.

When underwriters can price policies knowing that claims will be resolved with comprehensive visual evidence instead of battles over conflicting written interpretations, they can price more aggressively. They don't have to build in litigation costs, extended claim cycles, or ambiguity margins.

Reinspection costs drop. Claim cycle times shrink. Subrogation success rates improve because you have proof.

This changes how carriers validate their promises to policyholders. Instead of "you have to prove it" adversarial relationships or "we're just going to rely on our adjusters" opacity, there's a third option: shared visual truth.

As the broker, you become the one who eliminates the trust problem entirely. The data isn't subject to opinion. It is exactly what it is.

The carrier doesn't have to trust your client. Your client doesn't have to trust the carrier's adjuster. Everyone is looking at the same verifiable reality.

That's a fundamentally different value proposition than your competitors can offer.

Why Digital Twins Replace Expert Reports

This isn't future technology. This is current competitive reality.

The ability to remotely inspect a property through a Digital Twin has eliminated the need for physical visits in many insurance workflows. After storms, adjusters remotely inspect affected properties using detailed 360-degree views to gauge damages accurately and expedite claims.

Major players like Verisk are already deploying this at scale. Advanced technology enables eyes on site without boots on the ground to determine or verify key risk characteristics.

But here's what most brokers miss: This isn't just a convenience play. This is the replacement of written sampling reports with comprehensive visual documentation.

When you pull up a Digital Twin of your client's property in a carrier presentation, you're not showing them a prettier version of an inspection report. You're giving their experts the ability to conduct their own remote inspection based on comprehensive visual capture.

The underwriter can virtually walk the property. They can inspect every roof penetration using their own expertise and rating guidelines (not limited to what an inspector had time to photograph and describe). They can verify HVAC condition from all sides based on what they've been trained to look for, not based on what someone else summarized in text.

Written reports become unnecessary because experts can analyze the complete visual data directly.

In claims scenarios, this shift is even more dramatic. You become the broker who can prove pre-loss condition instantly with verifiable visual evidence. No arguments about what an inspector meant when they wrote "fair condition" three years ago. No litigation over conflicting written interpretations.

Just pull up the Capture Block and show exactly what existed before the loss.

That's not a nice-to-have capability anymore. That's table stakes for competitive insurance placement. Most brokers are still operating as if expert PDFs are the standard.

What Early Movers Understand That Others Don't

As of 2025, 67% of insurance firms are significantly accelerating their digital transformation initiatives. Those who still rely on legacy systems will get left behind rapidly.

But here's what most brokers misunderstand about "digital transformation": It's not about buying AI platforms or claims software. It's about replacing written sampling reports with comprehensive visual documentation as your foundation.

The brokers who understand this paradigm shift are building compound advantages right now.

They're not selling "better inspection reports." They're positioning themselves as the brokers who provide comprehensive visual documentation that any expert can analyze.

When you offer Property Blockchain™ methodology to your clients, you're offering something your competitors literally cannot match with traditional inspection services:

The ability to answer questions that weren't asked when the inspection happened.

Think about that for a moment. With traditional written reports, if the inspector didn't photograph something or write about it, that information is gone forever. You're locked into whatever they had time to document.

With comprehensive visual documentation, you can go back and analyze anything. A carrier asks about roof drainage patterns three months after the capture? Pull it up. A claim happens and you need to verify the condition of a specific area? Navigate to it in the Digital Twin and show timestamped proof.

You're not hoping an inspector happened to document what became important later. You captured everything, so any expert can analyze whatever matters when it matters.

This is what wins in insurance. Who has verifiable information when it matters. Who can prove what they're presenting instead of asserting it based on outdated summaries.

Think about what happens when carriers start preferring (or requiring) submissions with visual documentation programs. When they offer 5-8% better pricing because properties with active Capture Block™ programs have dramatically lower litigation risk.

The brokers who bring this capability to their clients in 2025 and 2026 will dominate their markets in 2027 and beyond.

The brokers who wait will find themselves unable to compete against verifiable truth.

The Competitive Timeline: Why 2025-2026 Matters

Eighty-six percent of agents report product availability challenges. Nearly 60% of agents report that more than half their clients now demand same-day quotes and policy issuance.

This pressure is forcing everyone to modernize. But most brokers are modernizing the wrong layer. They're buying better software to manage the same old written sampling reports.

The brokers who understand the paradigm shift are building data foundations that make them unbeatable.

Here's why the window is closing: Once carriers start recognizing that visual documentation programs eliminate 3-6% of their pricing uncertainty and dramatically reduce claim litigation costs, they will begin preferring (and eventually requiring) this level of documentation for competitive pricing.

The brokers who built visual data libraries for their key accounts in 2025 and 2026 will have multi-year Capture Block histories by 2027. They'll be able to show carriers time-series data proving maintenance quality, verify pre-loss conditions instantly, and demonstrate property improvements over time.

The brokers who wait will be starting from zero while competing against brokers who have years of verified visual truth.

Picture the renewal meeting in 2027:

Your competitor walks in with a complete Property Blockchain™ for the account: every HVAC unit from all sides with 18 months of condition tracking, every roof membrane with quarterly documentation proving maintenance, every square foot of the property in navigable 3D format with verifiable timestamps.

You walk in with a traditional inspection PDF from someone who spent four hours on-site last year.

Which broker do you think wins that account?

The race isn't "who adopts AI first." The race is "who builds the visual data foundation that makes AI valuable."

And that race has already started.

The Choice in Front of You

The paradigm has shifted from written sampling reports to comprehensive visual documentation.

Most brokers are still operating as if inspection PDFs are the foundation of property truth. They're not. They never were. They were just the best compromise we could afford given human bandwidth constraints.

Those constraints are gone.

You can bring comprehensive visual documentation to your clients now, while it's still a competitive advantage that differentiates you from every other broker in your market.

Or you can wait until carriers start requiring it and find yourself scrambling to catch up against brokers who have been building visual data libraries for years.

The brokers who understand they're replacing limited written reports with comprehensive visual documentation will dominate their markets.

The brokers who think this is just about prettier reports or fancier technology will get left behind.

By even reading this far, you're already ahead. The question is what you do with that understanding.

Because while everyone else is shopping for AI platforms to analyze their limited written reports, you could be building the comprehensive visual documentation foundation that experts and AI systems actually need.

The competitive timeline has already started.

And 2027 is closer than you think.