Five Jobs Crammed Into One: Why Adjuster Retention Requires Infrastructure Not Incentives

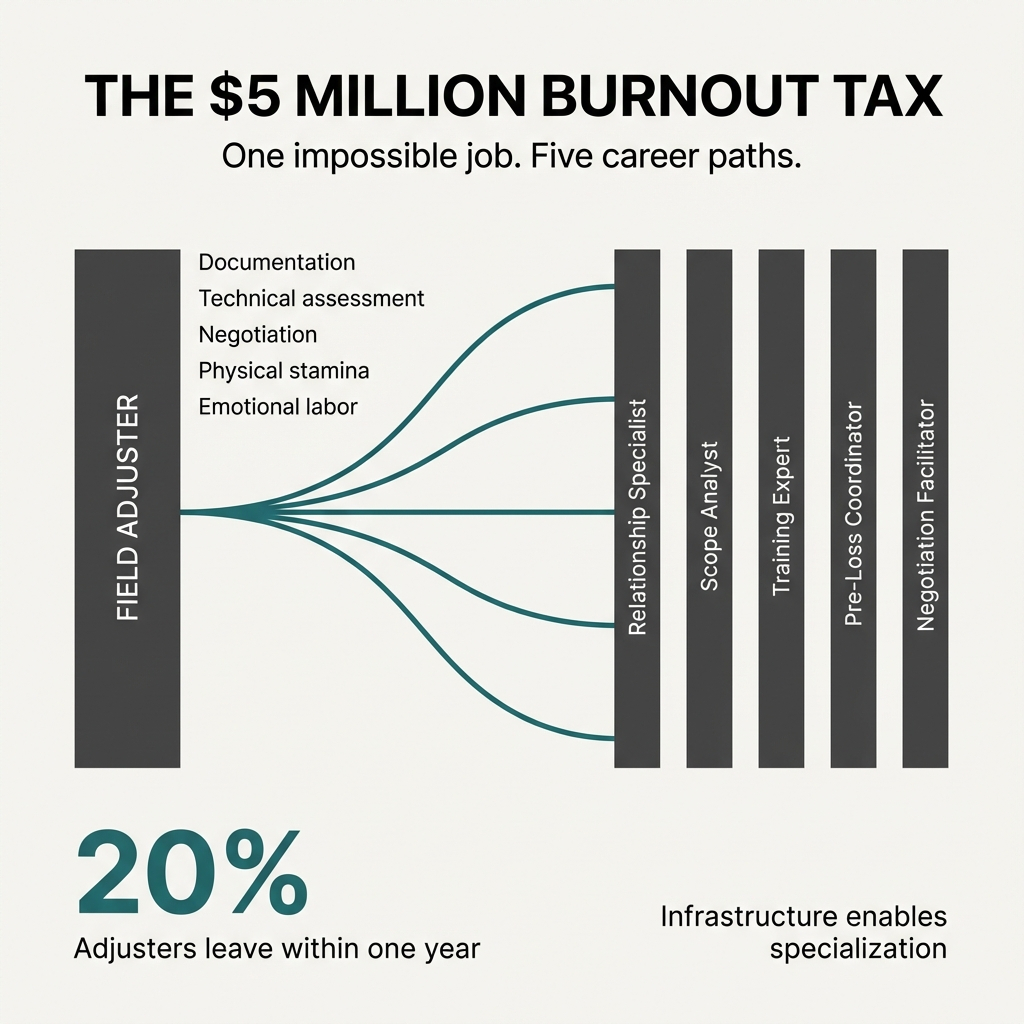

Industry research confirms what carriers already know. Adjuster burnout costs between $4,000 and $21,000 per employee per year. For a company with 1,000 employees, that's $5 million annually vanishing into turnover and lost productivity.

The average claims adjuster stays at their job for 1-2 years. Turnover rates exceed 20% in many regions. More than one in five adjusters leave within a year.

But here's the question carriers aren't asking: what operational infrastructure would make internal mobility and role specialization actually possible?

The Impossible Job Nobody Designed

The best field adjusters are valuable because of their face-to-face presence and judgment. They're the physical manifestation of the insurance promise. The 800-pound gorilla in the policyholder's corner when everything goes wrong.

But the current role bundles too many incompatible skills into one position.

You need interpersonal communication skills to handle emotionally charged situations. You need technical expertise to assess complex damage patterns. You need documentation precision to capture every detail. You need negotiation ability to reach fair settlements. And you need the physical stamina to climb ladders in summer heat while carrying equipment.

It's not one job. It's five jobs crammed into one role.

When carriers say "we need internal mobility," they're acknowledging the problem. When they fail to implement it, they're running into the operational barrier: knowledge transfer is nearly impossible when everything lives in one person's head and scattered PDF reports.

The Documentation Tax on Expertise

Right now, an adjuster shows up to a commercial property loss and starts crafting a narrative. They know that weeks later, sitting at their desk, they'll need to prove what they saw with photographs and notes. They'll need to defend their assessment. They'll need to justify their scope.

So they spend hours documenting. Taking photos. Writing notes about where each photo was taken. Trying to capture enough detail to remember everything later. Trying to anticipate what questions might come up in the future.

This is the hidden productivity tax.

Highly skilled professionals who can synthesize complex data and read damage patterns spend their time being professional photographers. They're forced into a generalist role when their expertise lies in specific areas.

The adjuster brilliant at complex negotiations still has to climb the ladder. The adjuster with incredible technical knowledge about structural damage still has to spend hours documenting routine measurements. The adjuster who excels at policyholder communication still has to worry about whether they captured the right angle on that HVAC unit.

What Comprehensive Visual Capture Actually Changes

When an adjuster arrives at a property where comprehensive visual documentation already exists, the entire job transforms.

They can focus on feeling the indentations in the siding. Reading the intangible signs a camera can't capture. Meeting with the policyholder, the contractor, and everyone with an emotional stake in the outcome. Building trust. Providing reassurance. Applying their expertise where it actually matters.

The night before the site visit, they're in their hotel room reviewing a complete digital twin.

They're tagging issues they see. Planning their day. Understanding scope before they arrive. Maybe AI did a first pass identifying potential damage. Maybe a junior associate flagged areas needing expert validation. The senior adjuster shows up knowing exactly what needs their attention.

They're not wasting time on site moving ladders and taking measurements. They're visiting three to five properties in a day instead of spending an entire day on one. They're force multiplying their expertise in the field, not getting pulled behind a desk.

This is what the Property Blockchain™ methodology enables. Comprehensive visual documentation captured by drones, 360 cameras, and trained surveyors. Every square foot documented. Every measurement geotagged. Every detail preserved in an unassailable source of truth.

The Emotional Labor Nobody Talks About

Dealing with upset policyholders is emotionally draining. The large number of claims, high customer expectations, and cost control pressures create significant burnout for adjusters.

But here's what changes when everyone works from the same digital twin.

The policyholder, their contractor, and the adjuster are all looking at the same comprehensive documentation. If the contractor wants to make sure the adjuster sees something specific, they can add their own photos to the digital twin through an app. Everyone knows exactly what everyone else is seeing and concerned about.

There's an emotional grounding in shared truth.

The adjuster isn't defending a subjective assessment anymore. They're facilitating collaborative problem-solving. The conversation shifts from "you're trying to screw me" to "okay, this is what was damaged, let's figure out the right scope."

When you have documentation from underwriting and every renewal, you can see exactly what changed. What was wear and tear. What was sudden and accidental damage from a covered peril. You remove the ambiguity that leads to adversarial dynamics.

The adjuster becomes a translator. Someone who helps coordinate scope of work and applies policy language to the actual situation. Not someone who has to defend their credibility while simultaneously trying to build trust.

The Trust-Free Tool

The camera lens is unbiased. It captures everything. It doesn't editorialize. It goes everywhere without fatigue.

You don't need to trust the surveyor. You don't need to trust the adjuster. You don't need to trust the policyholder. The digital twin simply is. It's reality, geotagged and time-stamped.

This removes the vectors for accusation. The adjuster isn't "some company shill denying for no reason." They're the professional who helps everyone understand what the policy covers based on what actually happened.

That emotional release alone creates an environment for productive discourse.

What the Job Actually Becomes

When baseline documentation is standardized, the differentiator between a good adjuster and a great adjuster becomes clear.

Communication. Coordination. Translation.

The job becomes specifying scope of work. Translating policy language to the actual situation. Walking people through how scopes are calculated and why. Doing it live with the policyholder if needed, clicking through the digital twin together.

In the age of AI-assisted text generation, the soft skills become even more important. Body language in virtual meetings. Empathy in emotionally tense situations. The ability to build trust when stakes are high.

These are the skills that can't be automated. These are where career growth actually exists.

The Career Paths That Emerge

Right now, adjusters have two options. Stay in the field doing everything, or leave the field entirely.

But when comprehensive visual documentation becomes the baseline, new specialized roles emerge:

- Field relationship specialists who focus on policyholder communication and contractor coordination, visiting multiple properties daily for high-touch interactions

- Complex scope analysts who work from digital twins, applying deep technical expertise to large commercial losses without the physical demands of field work

- Training specialists who use libraries of Capture Blocks™ to prepare new adjusters, dropping trainees into real scenarios before they ever visit a site

- Pre-loss assessment coordinators who review underwriting documentation and flag potential issues before claims even happen

- Negotiation facilitators who specialize in high-stakes settlements, using shared visual documentation to reach agreements faster

The adjuster who's brilliant at negotiation but burned out on travel doesn't have to leave the industry. They can transition to working from digital twins, applying their expertise to multiple complex claims simultaneously.

The adjuster who loves field work but struggles with technical documentation can focus purely on relationship building and on-site assessment while surveyors handle comprehensive capture.

Internal mobility becomes real because knowledge transfer becomes immediate.

When a 15-year veteran moves to a training role, they bring a library of Capture Blocks™ showing exactly how they assessed properties. New adjusters can walk through those same digital twins, learning to read damage patterns without months of shadowing.

When someone transitions from residential to complex commercial, they can study digital twins of industrial properties before their first site visit. They can see what experienced adjusters tagged as concerns. They can plan their approach based on comprehensive documentation.

The Deployment Path That Works

If you're a claims VP convinced this is the direction, start with your highest and best use.

Your most complex claims that are ongoing right now.

Multifamily properties. Warehouses. Industrial facilities. Properties that would take literal days to document with a guy on a ladder with a camera. Properties where you can't possibly capture every roof type, every HVAC unit, every window, every concrete slab in traditional reports.

Commission Capture Blocks™ for those properties. Make them part of your underwriting process. Instead of a property condition assessment, get a comprehensive digital twin.

Underwriters see what they're actually receiving. Claims professionals know pre-loss condition is documented. The chances of disagreement about what was damaged drop dramatically.

You can likely provide premium discounts to clients with Capture Blocks™ because your risk is lower. Your reserves can be deployed more accurately. It becomes a sales tool to grow your premium base.

Start the conversation with your underwriting VP.

If you both understand what a Capture Block™ entails and can prove the process is repeatable, you can streamline processes across the entire organization. You can defend decisions to senior leadership with visual evidence. You can demonstrate to stockholders that you're managing risk with precision.

The Infrastructure Internal Mobility Requires

Carriers know they need better retention strategies. The question is what operational infrastructure makes those strategies possible.

The answer isn't "hire more people" or "create better work-life balance policies." Those address symptoms, not causes.

The infrastructure is comprehensive visual documentation that preserves property truth over time. Capture Blocks™ from underwriting through every renewal. Digital twins that any qualified adjuster can access to understand a property without starting from zero.

This is what allows role specialization. This is what makes knowledge transfer immediate. This is what transforms the adjuster role from an impossible bundle of conflicting skills into a profession with actual career paths.

The technology exists. The methodology is proven.

What's missing is the recognition that adjuster burnout isn't just an HR problem. It's an operational design problem that requires operational infrastructure to solve.

Carriers that build this infrastructure will retain their best people. They'll create internal mobility that builds professional range instead of forcing binary choices. They'll transform claims processing from an adversarial grind into collaborative problem-solving.

The adjusters who stay won't be the ones who can tolerate the impossible job the longest. They'll be the ones who found the specialized role where their expertise creates the most value.

That's not an exit ramp. That's a career path.