February 2026: The Regulatory Ceiling Disappears

For a decade, the drone industry has been waiting for one thing: Beyond Visual Line of Sight regulatory clarity.

In February 2026, that wait ends.

The FAA is finalizing the BVLOS rule: the last major regulatory barrier preventing drone-in-a-box systems from scaling as permanent infrastructure. After that date, deploying networked autonomous drone systems shifts from regulatory nightmare to straightforward operational decision.

Most organizations think this is about delivery drones and Amazon packages.

They're missing the infrastructure revolution entirely.

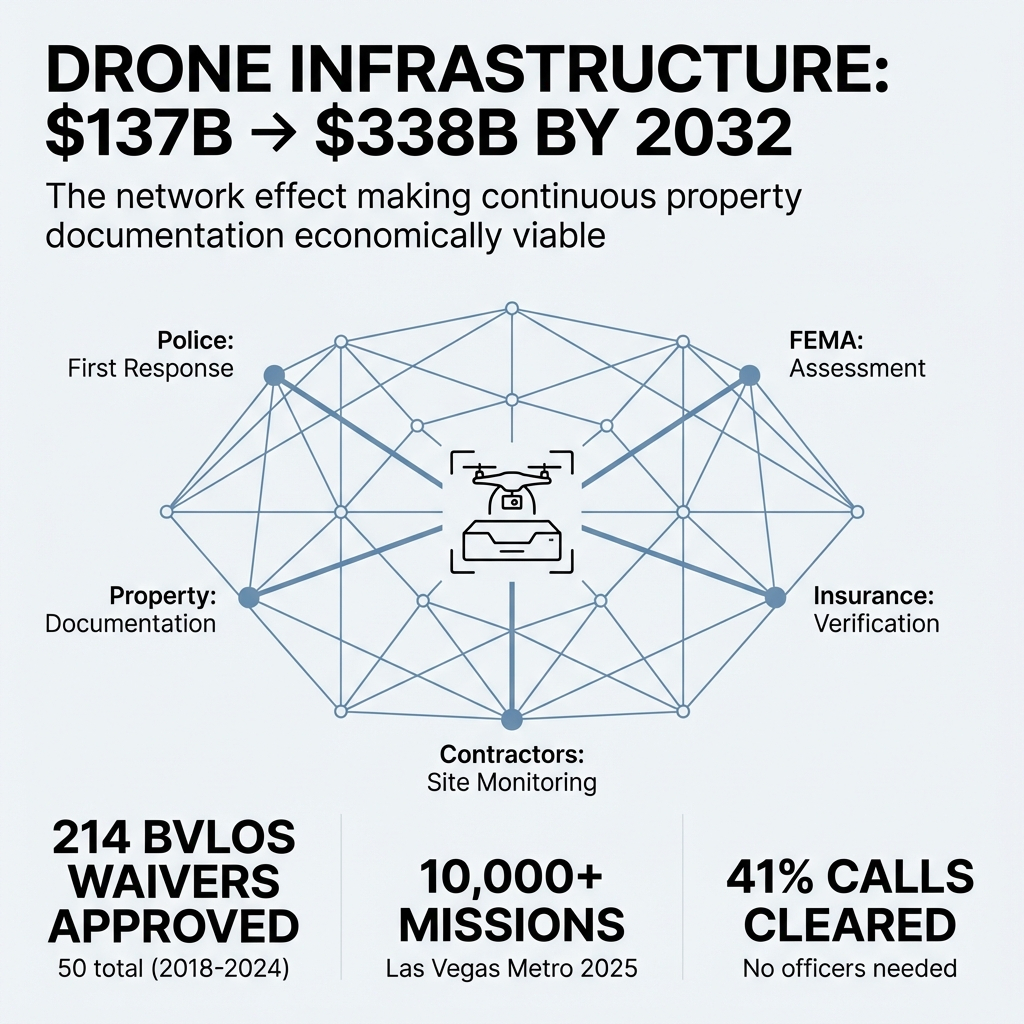

Between 2018 and 2024, the FAA approved only 50 Drone as First Responder programs total. As of June 2025 (after the waiver process was streamlined) there were 300 submissions with 214 approved.

That's not incremental growth. That's the dam breaking.

And we're just weeks away from the final rule publication.

What BVLOS Actually Unlocks

Beyond Visual Line of Sight means exactly what it sounds like: operating drones beyond where a human pilot can see them with their own eyes.

That doesn't sound revolutionary until you realize it's the difference between "expensive toy" and "scalable infrastructure."

Without BVLOS, you need a human pilot on-site or nearby for every operation. You need line-of-sight to the drone at all times. You can't cover large areas. You can't operate true networks. You can't deploy at scale.

With BVLOS, one pilot can monitor multiple drones across multiple locations remotely. You can cover entire city blocks, campus facilities, or commercial portfolios from a central operations center. You can automate routine missions and trigger deployments based on events.

You can build actual infrastructure.

The FAA streamlined the waiver process in spring 2025. Approval times dropped from up to a year to days. Then an executive order mandated final BVLOS rules by February 2026.

The regulatory ceiling that constrained the industry for a decade is disappearing.

What's Already Happening Before the Final Rule

Las Vegas Metropolitan Police Department flew more than 10,000 drone missions in 2025. Their Phase 3 deployment includes twelve locations with three docked drones each. If one drone's battery runs low during a call, another launches immediately.

That's not a pilot program. That's infrastructure.

Lakewood Police Department launched their program in March 2025 with one drone on one rooftop. In eleven weeks, it cleared 41% of calls for service without any officers needed. The drone arrived first 80% of the time.

Chula Vista's program: drones arrived on scene in less than 2.5 minutes across over 4,000 calls. In over 1,000 deployments, drone footage eliminated the need for dispatching a patrol unit entirely.

DFR programs have returned ground units to service in 25% of responses before officers even arrived on scene.

This is what's operational TODAY, under the waiver process, before the final rule simplifies everything.

After February 2026, the regulatory friction disappears. Deployment timelines collapse. Infrastructure buildout accelerates.

The Market Sees It Coming

The drone-in-a-box market was valued at $137.54 billion in 2025. Projections show it reaching $338.09 billion by 2032.

That's 146% growth in seven years.

That's not tool money. That's infrastructure money. That's the market betting on regulatory clarity enabling massive scaling.

And the money is betting correctly.

After hurricanes hit North Carolina in 2024, fourteen networked drone-in-a-box systems went live across one city. Police used them. Private businesses used them. FEMA used them. The Army Corps of Engineers used them.

Same hardware. Multiple users. Shared infrastructure.

That was the first city-scale networked drone system in the United States. It proved the infrastructure model works. It proved multiple stakeholders can share the same hardware. It proved the economics are viable.

That deployment happened under the old waiver system: the hard way.

After February 2026, doing that becomes straightforward.

Why This Date Matters More Than People Realize

February 2026 isn't just a regulatory milestone. It's the unlock for everything that's been waiting in the wings.

Right now, organizations exploring drone infrastructure face eighteen months of regulatory compliance before flying their first mission. After February 2026, that timeline collapses to weeks.

Right now, deploying networked systems requires navigating FAA waivers, compliance documentation, and operational limitations. After February 2026, those barriers largely disappear.

Right now, the infrastructure buildout is happening through early adopters willing to fight through regulatory friction. After February 2026, mainstream deployment becomes viable.

The technology is ready. The economic model is proven. The use cases are established. The only thing holding back infrastructure scaling has been regulatory clarity.

That clarity arrives within weeks.

What Applications This Enables

Here's what becomes viable after the regulatory unlock:

Continuous visual documentation of physical assets at scale. Properties, facilities, construction sites: comprehensive visual records captured on regular schedules without prohibitive costs.

Rapid incident response for security, safety, and emergency situations. Drones arrive on scene before human responders, providing real-time intelligence.

Preventative monitoring for infrastructure, equipment, and facility conditions. Issues get identified before they become failures.

Operational visibility across dispersed portfolios. Decision-makers can visually inspect multiple locations simultaneously without travel.

Risk verification for insurance, lending, and investment decisions. Pre-loss conditions become verifiable facts instead of disputed opinions.

These applications exist today. What changes after February 2026 is the economics and timeline for deployment.

What required eighteen months and six-figure investments becomes accessible in weeks through shared infrastructure networks.

The Public-Private Infrastructure Model

Here's the model that I feel makes this economically viable at scale:

Public safety organizations deploy drone-in-a-box networks for first responder operations. Those deployments get justified by force multiplication, faster response times, and officer safety benefits.

That infrastructure then becomes available for commercial uses during downtime. Property documentation. Security monitoring. Construction progress tracking. Facility inspections.

A single drone-in-a-box system costs $50,000 to $150,000 depending on configuration. Add maintenance, regulatory compliance, staffing, and data processing, and one organization is looking at $200,000+ annually to operate.

That's prohibitive for most.

But when five organizations share infrastructure, you're looking at $40,000 per organization annually. When ten organizations share it, that drops to $20,000.

The public sector justifies the infrastructure buildout. The private sector leverages that infrastructure for commercial applications. Hardware utilization approaches 100% because the system is always working for someone.

This model only works at scale with BVLOS operations. Without BVLOS, you can't cover areas large enough or operate networks efficiently enough to support multiple users.

After February 2026, that constraint disappears.

The Pre-February and Post-February World

Before February 2026, deploying drone infrastructure is possible but painful. It requires navigating waivers, accepting operational limitations, and fighting through regulatory uncertainty.

Early adopters are doing it anyway because the value is undeniable. Las Vegas, Chula Vista, Lakewood, North Carolina: these deployments are happening under the old system.

After February 2026, the friction disappears. Deployment becomes operationally straightforward. The timeline collapses from eighteen months to weeks. The regulatory uncertainty evaporates.

That's when mainstream adoption accelerates.

Organizations positioning themselves now (building partnerships, understanding the infrastructure model, identifying use cases) will be operational before their competitors understand what's happening.

Organizations waiting for "proof of concept" or "mature technology" will discover the infrastructure is already deployed and they're negotiating access at whatever terms the market offers.

This isn't speculation. This is pattern recognition from every infrastructure transition in history.

What I'm Watching For

Here's what I think happens after February 2026:

March - June 2026: Infrastructure providers race to deploy under the new simplified rules. Cities that have been waiting on regulatory clarity start procurement processes. The deployment pipeline that's been artificially constrained starts flowing.

Second Half 2026: At least thirty major cities will have operational drone-in-a-box networks, primarily purchased by municipalities. Commercial access to those networks might emerge but remain poorly understood by most organizations.

2027: Commercial applications scale as organizations realize they could access existing infrastructure instead of building dedicated systems if given permission by the owning entity. Insurance companies begin differentiating pricing based on properties with continuous documentation capability versus traditional sporadic inspections or fixed wing resolution limitations.

2028: The network effect accelerates. Properties without infrastructure access face measurable disadvantages in insurance costs, capital efficiency, and operational visibility. Late movers scramble to secure access and discover capacity is constrained.

2029-2030: Continuous visual documentation of significant physical assets becomes standard practice, not innovative edge case. The question shifts from "Should we do this?" to "Why didn't we start in 2026?" The visual information layer becomes key to unlocking robotics at scale and really making the world “feel” like the future!

This trajectory assumes the February 2026 timeline holds. If it slips, everything shifts accordingly. But the direction doesn't change. The regulatory unlock is coming. The infrastructure buildout follows immediately after.

Why Most Organizations Will Miss This

Most organizations are still thinking about drones as tools, not infrastructure.

They see drone deployments as capital purchases: hardware you buy, pilots you train, operations you manage internally. That framing makes the investment look prohibitive and the timeline look daunting.

They're missing the infrastructure access model entirely.

The organizations that understand this aren't buying drones. They're positioning themselves to access infrastructure networks that are being deployed for other purposes. They're identifying where drone-in-a-box systems will be operational for public safety and negotiating commercial access during downtime.

They're asking different questions:

"Which cities in our operating footprint are deploying DFR programs?"

"What commercial applications could we run on that infrastructure?"

"What would continuous visual documentation enable for our operations, risk management, or capital allocation?"

"What partnerships do we need to build now to ensure access when those networks go live?"

Those questions separate early participants from late adopters.

And after February 2026, the gap between those two groups widens dramatically.

The Bottom Line

February 2026 is the regulatory unlock the drone industry has been waiting for since autonomous systems became technically viable.

After that date, the barriers to deploying drone-in-a-box infrastructure at scale largely disappear. Timelines collapse. Economics improve. Mainstream adoption becomes viable.

The infrastructure buildout that's been artificially constrained for a decade accelerates immediately.

Public safety organizations will deploy networks for first responder operations. Those networks will create infrastructure capacity that commercial operators can leverage. Shared infrastructure models will make applications economically viable that were impossible as standalone investments.

This isn't speculation about the distant future. This is description of what should happen in a matter of weeks.

The organizations paying attention are positioning themselves to access that infrastructure as it comes online. The organizations not paying attention will discover the infrastructure is already deployed and they're negotiating access at whatever terms the market offers.

The regulatory ceiling disappears in February 2026.

What you do right now determines whether you're an early participant or a late adopter.